Presentation

Since 2018 Pebay gladly publishes its Price & Performance report,

revealing exclusive data that uncovers the true performance, in local

currency, of private equity funds as well as the price these funds are

paying to acquire companies in Brazil. Every year our report

concludes with a case study of a successful deal done in Brazil to

illustrate what happens at the micro level and inspire those looking

to venture into private markets in search of superior returns. While

investing in private markets carries greater risk, especially in

developing countries, the well informed investor will always be

better positioned to find the hidden gems and avoid the pitfalls along

the road.

Price & Performance of Private Equity in Brazil

Information on private equity entry price and fund performance is

tremendously important for those navigating through private capital

markets.

Market level performance metrics such as Internal Rate of Return

(IRR) and Total Value to Paid-In Capital (TVPI) are key for Limited

Partners (LPs) to decide their allocation plans, select the best funds

and managers and monitor their portfolio properly. It also helps

understand the impact of different economic cycles on funds, as well

as decide to sell or buy in the secondary market of funds.

Price metrics such as Enterprise Value (EV) to Earnings Before

Interests, Taxes, Depreciation and Amortization (EBITDA) and Equity

Value to EBITDA are also key for General Partners (GPs) to benchmark

against peers and know how close or far-off their multiples are

comparatively to the market. With that in mind, LPs can also assess

the discount of private versus public equity alternatives.

With access to price and performance data, buyers, sellers, advisors

and investors face less uncertainty and can better understand the

source of performance, being able to act in order to improve it. As a

result, more capital can flow into the market, with more liquidity and

better returns.

However, price and performance information is extremely hard to

come by. Let alone find unbiased information about it. This is due to

many factors:

- Opaque market: Private fund and deal information are usually kept private;

- Inaccurate news and gossip: Press releases and news articles tend to be biased towards bigger transactions that make it to the headlines, not always reflecting the true transaction values and participation acquired. Usually news do not bring complete and accurate financial information at company level, such as EBITDA or net debt (which are used to calculate EV);

- Biased fund performance: Fund performance information are usually made available by GPs in fundraising mode, creating a natural bias towards disclosing information about the most profitable funds and deals;

- Currency effect: The information usually available regards funds that catered to public pensions funds abroad, and is dependent on disclosure by foreign LPs that only provide the information in their own currency (generally US Dollars or Euros). Given the large fluctuations of emerging markets currencies, this can severely distort true results.

Pebay compiles data on funds, investment vehicles and companies

from several regulatory sources in Brazil. This data then undergoes

handcraft analysis from a group of specialized analysts. The result is

a complete performance set of more than 830 funds and club deals

in Brazil (1) launched from 1995 to 2019. In-depth analysis was

performed based on the financial reports of over 1,370 out of 2,355

companies that received investment from these funds.

The cash flow information needed was based on audited financial

reports and regulatory filings. Omissions, missing information or

uncertainties were identified and treated directly with fund

managers, administrators and LPs.

Note on IFRS 16

The International Accounting Standards Board (IASB) issued IFRS 16 which is in effect for financial periods beginning in 2019. IFRS 16 forces companies to recognize the net present value of leases as an asset – “rights of use”; and as a liability – “lease liability” which generates “interest” expenses (the lease installments) and amortization. This change is causing an increase in the following metrics without impacting cash flows: (i) Net debt, as the lessee will recognize the “interest-paying” liability for the lease; and (ii) EBITDA, as the lessee will recognize the interest cost and the depreciation of the leased asset instead of the operating lease expenses. Companies with high lease expenses are especially affected, such as retailers. As a consequence EV/EBITDA and Net Debt/EBITDA for 2019 tend to be higher than they would be under the former methodology.

Performance

The results below show the true performance of private equity funds

and club deals by vintage, in local currency (BRL).

It is important to highlight that some regulated funds charge

management fee and performance fee locally and others charge it

abroad. So to compare apples to apples, the performance was

analysed on grossed-up terms. It means that fees charged in Brazil

were added back to cash flows to allow full comparability. Also, for

pan-regional funds, or global funds, only the portion invested in

Brazil was included in the analysis.

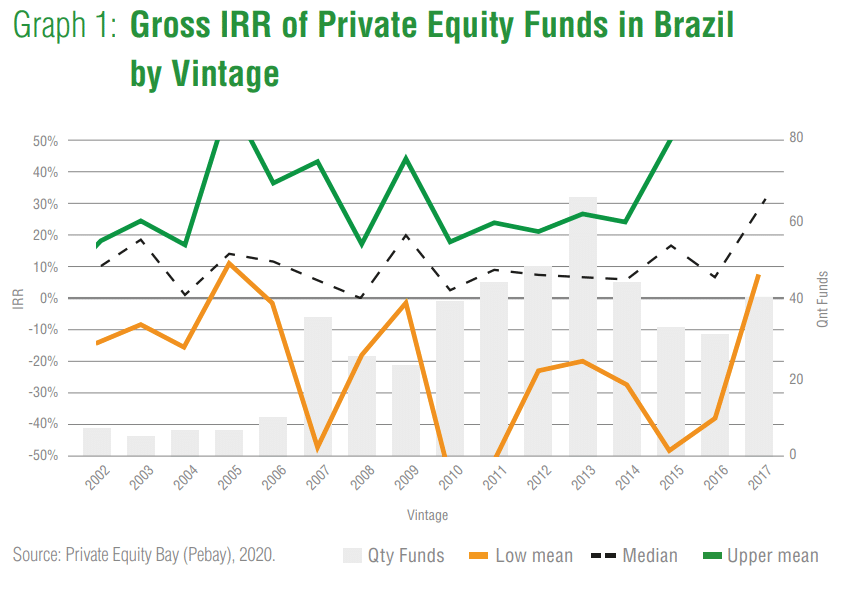

Gross IRRs in Brazil runs around 10% p.y., a relatively low figure for

a country that only saw its sovereign interest rate (Selic) fall below

10% on three occasions in the last 18 years: 2009 (8.7%); 2012

(7.1%); and from 2018 on (2% in 2020).

Exception to the norm was the following especially good vintages:

2003, 2005, 2009 and years from 2015 on. In particular, 2003 and

2009 benefited from a crisis in the previous year, resulting in median

IRR around 20% p.y. In 2005, the market was starting to witness a

continuous expansion in liquidity and Initial Public Offerings (IPO) that

lasted for five years. That brought the median IRR up to nearly 14%.

In 2015-2016 Brazil suffered a serious economic and political crisis

with a sluggish recovery in the 2017-2019 period (around 1% GDP

growth p.y.). Interest rates came down from 13.75% in 2017 to 2% in 2020.

While Covid-19 harmed the economy even further, it also

helped foster technology-based companies and the number of

investors in the stock market (which grew from 1.9 to 3.1 million

investors). The search for higher yields helped the stock market

quickly recover and opened an IPO window that allowed 25

companies to go public, raising R$31 billion (second highest volume

ever, losing only to the 2007 IPO rush). Other 45 companies have

filed for IPO and are expected to go public in the next few months.

The combination of high liquidity, diminishing cost of capital and IPO

window coupled with the possibility to make investments after the

crisis has brought IRR up in the last few years: a median of 15% in

2015 and 2016; 30% in 2017.

While performance of 2017 vintage should still change over time

(five years is the advisable time-span to evaluate PE performance), a

great part of this early outperformance can be explained by the quick

reduction of interest rates in the last 3 years, which contributed to a

steep increase in the value of assets in general

(2).

Infrastructure investments with long and predictable cash flows are

particularly prone to this effect. These funds have become very popular

in the last four years in Brazil. According to Pebay.info data, in 2016

“Infrastructure” funds represented 17% of the industry’s aggregate

value. By September 30th 2020 this figure increased to 33%.

Good vintages also have another important feature. Not only returns

get better, but the risk is reduced. For example, in 2005, even the

bottom performers had 11% IRR on average. As for 2009 and 2017

vintages, bottom performers had IRR of -3% and 9%, respectively.

The results suggest that timing the market can be very helpful for

private equity investors. Investments made after the crisis and just

before a period of liquidity and IPO have shown significantly better

risk-adjusted returns.

Looking at the average of the top half performers and the bottom half

performers another relevant conclusion emerges. Until 2004 the top

performance was not too far apart from median performance. In

2003 for example the difference in IRR was barely noticeable. From

then on the gap widened, making top performers always hover above

15% (also above the prevailing interest rates), reaching heights of

63% in 2005, 45% in 2007 and 2009, and 78% in 2017.

The widening in performance among managers is consistent with the

idea that fund managers do get to differentiate over time based on

experience, reputation, access to capital, strategy, execution etc. This

is especially true for a young PE market such as Brazil. These are

major factors behind discrepancy of returns.

2014 is a good example of that. When bottom performers were

posting -49% IRR (losing almost two-thirds of capital invested), top

performers were, on average, posting 29% IRRs: a difference of

7,800 basis points!

In a market that looks like that, it is the manager/fund selection skills of

an LP that determine how successful or unsuccessful its private equity

program will be. With the only exception of 2005 (2017 is still too early

to tell), if one was unlucky enough to invest with the bottom performers

(and only them), money would have been lost on every vintage.

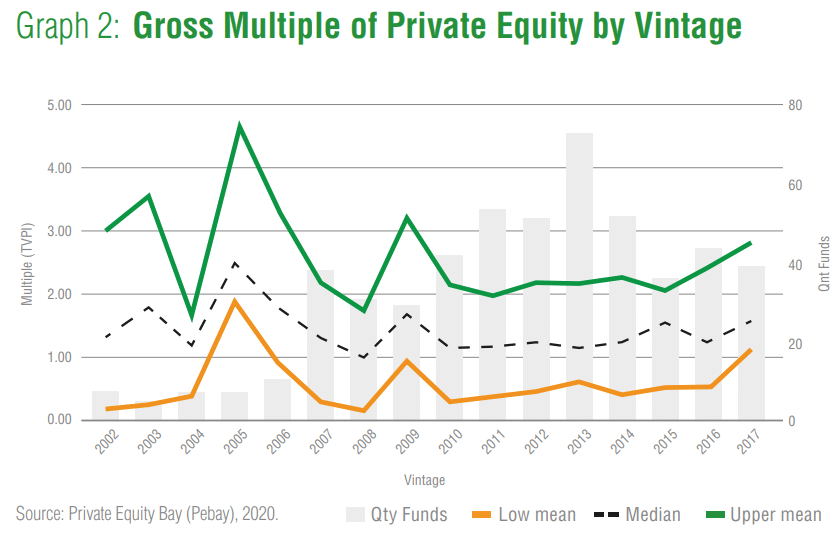

The performance was also analysed with multiples of capital invested

(see Graph 2). In line with IRR analysis, it shows median running

around 1.5x up to 2009, dropping to 1.15 ~ 1.20 afterwards, then

increasing to 1.5x in 2015 and 2017. It reached above 1.75x in four

moments: 2003, 2009 and at the beginning of the liquidity/IPO boom

in 2005/2006. For these vintages top funds had on average 3 to 4.5x

multiple on invested capital.

This analysis of multiples is especially useful to measure downside

as it shows for instance that low performers can, on average, lose

50% of capital. Or, lose virtually all capital as it was the case in 2002,

a vintage severely hit by the Internet bubble burst; and 2010, a point

of inflexion in the economy that ended up affecting many portfolio

companies and projects.

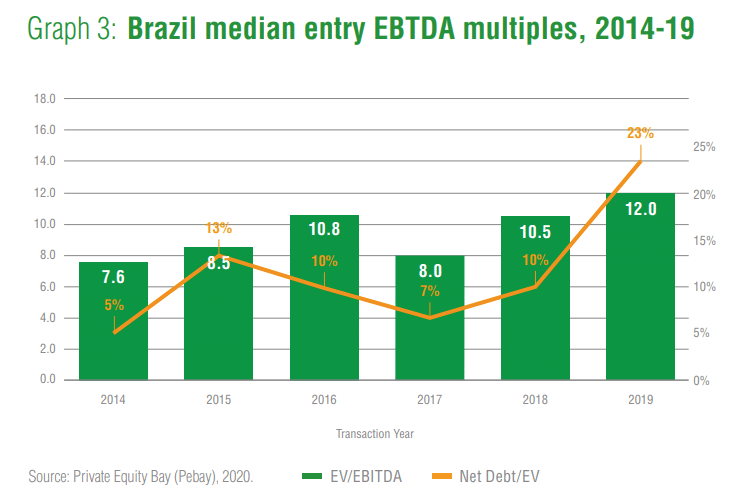

Price

Private Equity transaction entry price is another key piece of

information to understand the attractiveness of a private market. It is

something certainly known to the acquiring fund, the seller and its

advisors, but rarely publicised.

However, in Brazil corporations (Sociedades Anônimas – S.A.) are

generally obliged to publish financial information on an annual basis.

So by identifying the corporations in the portfolio of each fund (either Looking directly or indirectly under holding entities), Pebay was then able to handpick financial

reports of the portfolio companies to calculate accounting EBITDA

(without adjustments) and Net Debt of the same year the initial

investment took place. Whenever possible, consolidated

information was obtained on the higher available holding entity.

Results show that EV/EBITDA in Brazil range around 7.6x to 12.x, with

net debt representing 5% to 10% of EV, except for 2019 when this

figure reached 23%, perhaps as a result of the lower interest rates

and IFRS 16.

Despite the peak in 2019, a foreign investor looking at Graph 3 would

be intrigued to see how little debt is used by private equity invested

companies in Brazil when compared to US and European companies.

Until recently Brazil has had relatively high interest rates and a

concentrated banking industry. So medium and small size companies

in Brazil used to face interest rates of 25% to 30% p.y. Gladly the

financing gap has been fulfilled by the private equity industry. Now

medium companies have access to debt at much lower rates.

| Box 1: Investing successfully in the Brazilian e-commerce logistics sector 2020 was marked by the outspread of Covid-19 which has sadly taken many lives and changed the way we live. Thanks to technology society was better prepared to face such a tremendous challenge. Broadband, apps with online chat/video services and streaming helped us stay connected, entertained and educated. E-commerce platforms allowed big and small shops to start selling online quickly while helping the population cope with stay-at-home policies by having services and goods delivered at home. Brazil has a large territory and online customers accustomed with seamless digital experiences demand increasingly shorter delivery times. This creates a huge opportunity for logistics companies specialized in online retail that can reach Brazil’s farthest corners such as private-equity-backed Sequoia Logistica (SEQL). Present in more than 3,359 cities that represent 92% of the Brazilian GDP, the company rose to the challenge and was able to grow considerably (80% in the nine first months of 2020), allowing it to make its successful debut in the Brazilian stock exchange (B3) in October 2020, with outstanding returns for its existing and new investors. Founded in 2010, SEQL is one of the leading tech-enabled logistic companies in the Brazilian e-commerce, with 16% market share3. Between 2014 and 2019, its net revenue and EBITDA increased at an annual growth (CAGR) of 24% and 29%, respectively. In 2019 it made 30 million door-to-door deliveries and over 1.4 millions same-day deliveries, totalling R$527 mn in net revenues and R$65 mn in EBITDA. The company has an asset-light business model: 98% of its fleet is either outsourced or leased, allowing it to post a 34% return on invested capital (ROIC). In 2014, the company attracted private equity investment from global growth capital manager Warburg Pincus (WP), a group with a strong tech-enabled logistics expertise that has invested over U$86 bn in more than 930 companies around the world. As a result Sequoia has achieved a long-term strategic plan which included revision of its brand concept, implementation of a meritocratic culture and improvement in corporate governance and internal controls. SEQL fostered its M&A capability. Six acquisitions were made in the last eight years, which allowed the company to access new States and verticals such as fashion and financial services. WP invested a total of R$171 mn in the company, valuing SEQL’s equity initially at R$194 mn. Company had around R$18 mn in EBITDA and R$54 mn in net debt, resulting in an EV/EBITDA of 14x and EV/Revenues of 1.4x. WP amassed a total stake of 70.5% before the IPO, which allowed the fund to reduce its stake to 21.7% and recoup R$522 mn, or over 3 times the amount invested. The remaining stake was valued at almost R$342 mn at the IPO price, thus resulting in an interim multiple of invested capital (MOIC) of 5.0x and a gross IRR of 39%. SEQL’s IPO came in a rare moment when the market was receptive to new listings, even though global economic uncertainty was still high (i.e. US Elections and the possibility of a second wave of Covid-19 lockdowns). Price was set at R$12.4/share, below the range of R$14.25 to R$17.15, giving the company a market cap of almost R$1.6 bn, which translates to a multiple of 18.5x EV/EBITDA (twelve months up to September 2020). Investors that bought shares in the stock market saw their investments rise nearly 60% in 2 months, making it a top performing IPO of 2020. There is great expectation about the sector’s future. According to Ebit and Forrester, e-commerce in Brazil is expected to increase by approximately 250% (CAGR of 23%) until 2025, reaching R$377 bn in sales volumes. At 7.2%, the penetration rate of e-commerce in Brazil to total retail is much lower than in more developed countries. In China and in the US penetration is 27% and 15%, respectively. It is reasonable to expect a good performance for the sector in the next few years. However competition should be fiercer. Big marketplaces such as Mercado Livre have developed proprietary logistic networks to insure quality and increase same-day-delivery. Brazilian government is also preparing to privatize Brazil’s post service (Correios) which is SEQL’s main competitor with 33% e-commerce market share. While present all over Brazil, Correios suffers with management issues, recurring employee strikes, poorer client service, making its delivery time slower and less reliable. This could well change once the service falls in private hands. |

About Private Equity Bay (Pebay)

Private Equity Bay (Pebay) maintains an online private equity

intelligence service (Pebay.info) specialized in PE, Real Estate,

Infrastructure and similar investments in Brazil. Pebay tracks and

analyses performance of more than 1.040 funds, of 415

managers, as well as more than 2.900 invested companies and

projects with data on investments, financials and valuations. All

based on the highest standards of quality and reliability. With Pebay

investors can better monitor their investments, compare

performance, originate opportunities, access the secondary market

and reduce time spent with search and treatment of information.